Pay with cash, preserve freedom

⚡Key Takeaways

- Cash is more than a means of payment: it protects privacy, freedom, and sovereignty in an increasingly digital financial world.

- Every cashless payment creates data points that can be turned into profiles, scores, and potentially into control or exclusion.

- Digital ID and biometric payment systems can quickly turn “inclusion” into exclusion when access to participation is tied to identity.

- De-banking shows how dangerous a cashless order is: accounts and payments can be technically turned against unwanted individuals with ease.

- Cash limits the market power of Visa, Mastercard, and other payment networks and protects merchants and consumers from rising fees.

Why I Do Without Card Payments When I Take Freedom Seriously

We often talk about convenience, efficiency, and digitalization — but far too seldom about power. That is exactly where, for me, the real debate about the abolition of cash begins. Cash is not just a means of payment. It is a piece of lived freedom, a final analog shield in an increasingly transparent financial world. Anyone who casually says today, “I only pay by card,” should ask themselves a simple question: Do I want convenience — or do I want sovereignty?

I say this quite deliberately: If I can afford it, I consciously pay in cash. Not out of nostalgia. Not because I am hostile to technology. But because cash is the price of freedom — small, inconspicuous, in your hand every day, and precisely for that reason so valuable. In a world where every payment can become a data point, every purchasing pattern a profile, and every account movement a potential lever, cash is not a relic. It is a bulwark.

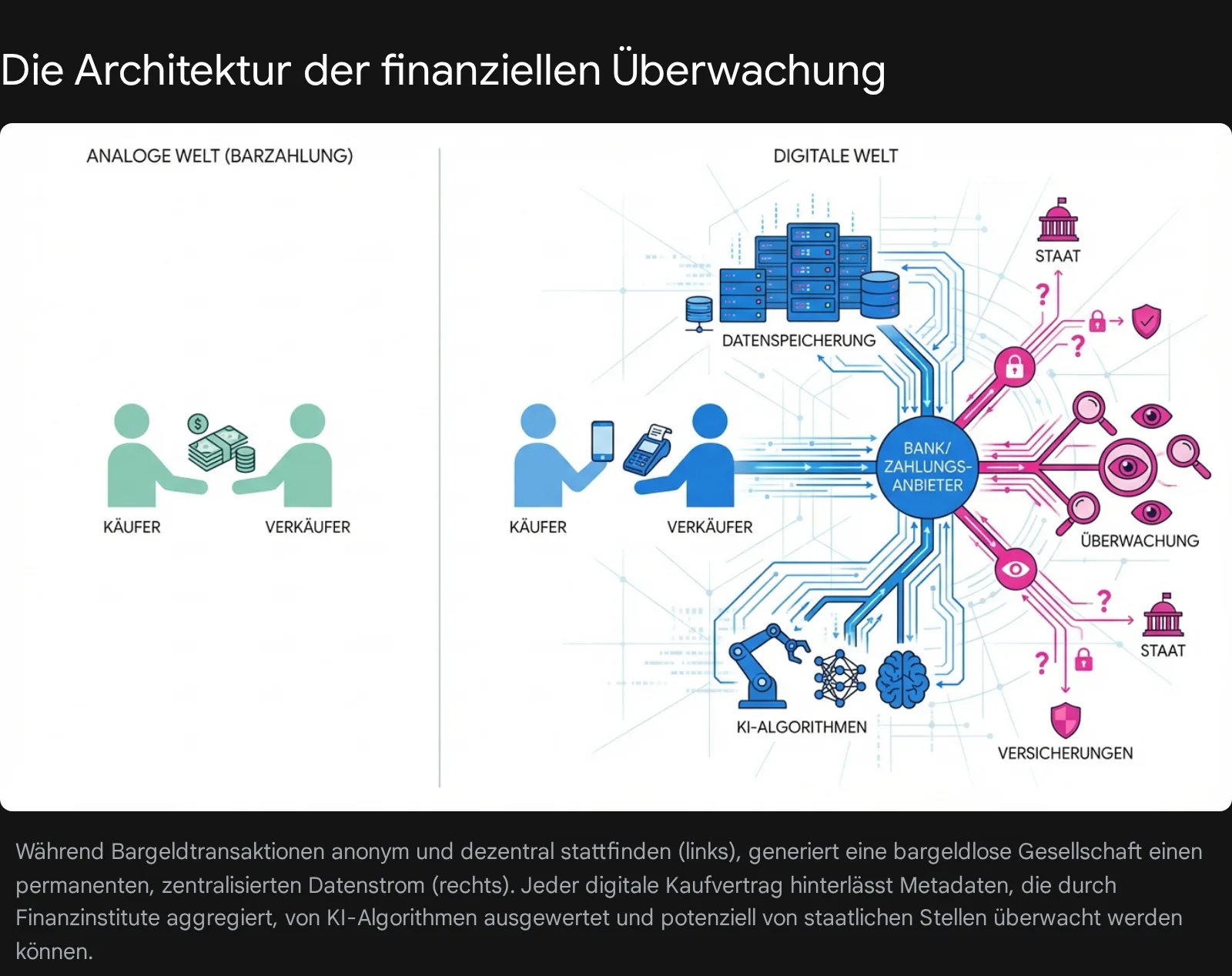

Why Cash Is More Than Just Banknotes and Coins

In my view, cash is far more than the physical counterpart to a digital transfer. It is a bearer instrument: You own it, you pass it on, done. Without an intermediary. Without an app. Without approval. Without biometric verification. It is precisely this simplicity that makes cash so democratic.

The deep research findings show very clearly what the trend toward a cashless society is really about: not just efficiency, but the reshaping of the entire social contract. If every payment transaction runs only through banks, payment service providers, or state-controlled infrastructures, then a simple exchange process becomes a permanently monitored, steerable, and analyzable process. That is not a small technical change. That is a shift in power.

The 10 Most Important Arguments Against Abolishing Cash

Here is my short but clear summary of the strongest reasons why cash must remain:

Privacy: Cash prevents every purchase from becoming a data record.

Freedom: You can pay without having to identify yourself.

Protection from surveillance: Cash stops complete financial profiling.

Protection from de-banking: If you have cash, you are not completely dependent on the banking system.

Crisis resilience: Cash works even without electricity, internet, or servers.

Competition: Cash curbs the power of Visa, Mastercard, and the like.

Lower costs: Without cash, card fees and merchant prices rise.

Social participation: Cash is more accessible for older people and people without digital means.

Protection against forced digitalization: Digital ID and mandatory biometric checks can create exclusion.

Democratic emergency exit: Cash remains an analog escape route from an overcontrolled payment order.

Share this article with friends and relatives and preserve cash!

The Greatest Loss: Financial Privacy

Every Payment Becomes a Record

For me, the most important point is privacy. In a cashless world, every coffee, every book, every donation, and every tank of fuel becomes a permanent data point. That sounds abstract, but in reality it is brutally concrete: consumer behavior becomes profiles, profiles become ratings, and ratings become decisions.

Research rightly points to the danger of algorithmic profiling, “guilt by association,” and the silent linking of transaction data with sensitive information. Anyone who regularly pays at pharmacies, medical facilities, or certain merchants may trigger inferences about health, lifestyle, or financial stability — without ever having consciously consented to it.

For me, that is the core of the matter: Cash protects not only against the state, but also against the total commodification of human beings.

A Powerful Metaphor for What Is at Stake

Cash is like the last open window in a house that is being locked down, wired up, and monitored more and more tightly. If you close it because the heating seems sufficient, you may only later realize that you are already sitting in the air-raid shelter of a digital panopticon. Comfortable, warm — but without fresh air, without an escape route, without privacy.

Digital ID and Biometric Systems: When Access Becomes Mandatory

The deep research examples from Vietnam and Nigeria are particularly revealing. They show how easily “financial inclusion” can become a massive form of exclusion. In Vietnam, according to the information available, millions of accounts were made dependent on biometric verification. Anyone who was not properly verified lost access to digital transactions. In Nigeria, the central bank tied banking access to BVN and NIN — with partly catastrophic consequences for people living in rural areas or lacking stable infrastructure.

What alarms me most about this: On paper, such systems always sound like order, security, and modernization. In reality, however, they create a new class of dependency. If money works only with digital identity, then identity itself becomes a lever of control. And if the infrastructure is missing, “inclusion” suddenly turns into exclusion.

For me, that is a central warning: A financial system must not become a biometric gateway to participation in life.

De-Banking: When Money Is Used as a Political Weapon

Perhaps this is one of the most unsettling arguments against a fully cashless world: Financial exclusion of politically unpopular people becomes technically easier all the time.

The examples range from Russia to Hong Kong to Canada and the United Kingdom. Accounts were frozen, access cut off, payments blocked — often with vague justifications, sometimes with an openly political agenda. The problem is not just the individual case. The problem is the structure behind it: if cash disappears, access to a bank account becomes the gatekeeper for almost everything.

What is sold today as “compliance” can tomorrow become an instrument of discipline. And that is exactly why I consider de-banking so dangerous: It is clean, quiet, and often difficult to challenge. No open blow, but an economic bleed-out.

My stance on this is clear: A free society needs a means of payment that cannot be turned against dissenters at the click of a button.

The Fee Trap: Why Cash Also Protects Your Money

Visa, Mastercard, and the Duopoly Problem

Another point that becomes clear in the research report is the economic power of private payment networks. Visa and Mastercard dominate the market in many countries, and when cash disappears, merchants lose their most important bargaining chip. Then they are largely at the mercy of these networks’ fee structures.

The British market review showed rising fees even though no corresponding increase in costs was evident. That is exactly the point: without cash as a real alternative, price increases can take on a life of their own. In the end, not only do you as a consumer indirectly pay more, but small merchants also lose margin and freedom.

I like to translate that into a simple formula: Less cash means more power for payment platforms and higher costs for everyone else.

The Silent Tax on Every Purchase

Fees in digital payment traffic are often invisible. They do not appear as tax, but they work much the same way. And the less cash there is in circulation, the less the market can discipline these fees. This is not a theoretical risk — it is already reality in many countries.

Why Cash Remains Unbeatable in Crises

Digital systems are convenient, but they are also fragile. The examples of the Visa outage in 2018, the TSB debacle, the CrowdStrike fallout, and various cyberattacks on payment service providers prove that. When servers fail, when software updates go wrong, or when hackers strike, the entire payment architecture can come to a sudden halt.

Cash, by contrast, is robust. It needs no battery, no network, no authentication, and no third party. A power outage does not erase a banknote. A server crash does not suddenly turn 20 euros into 0 euros.

That is precisely why I see cash as a kind of disaster-proof emergency exit. In normal times, it is underestimated. In an emergency, it saves you.

India 2016: A Textbook Case for the Risks of Abrupt Cash Policy

Demonetization in India is, for me, the most striking historical example of how destructive state intervention in the cash cycle can be. Overnight, 500- and 1,000-rupee notes were invalidated. The goal was to fight corruption and the shadow economy. The result, however, was massive chaos, a shortage of liquidity, job losses, and enormous strain on millions of people — especially in the informal sector.

Research also shows that the big black-money hit failed to materialize. A large portion of the money returned to the system. What remained was mainly the collateral damage to the people who depend on cash.

And something else is important: Such measures often accelerate digitalization not voluntarily, but by shock. That means: not the best solution wins, but the only one still available. That is how habits are broken.

For me, India is therefore a warning with emphasis: When cash is politically devalued, it is not the powerful who pay the price, but ordinary citizens.

Why I Pay in Cash on Purpose When I Can

Here my personal position is laid out quite openly: I see cash as a daily vote for freedom. Not because card payments are inherently evil. Not because digital payments are always bad. But because I know that convenient systems are rarely neutral.

When I pay in cash, I make a small but clear decision: I consciously give up some of the data traces, a bit of convenience, and sometimes even a minimal gain in comfort. But in return I buy something more valuable: independence.

I believe we should relearn that. Not dogmatically, not fanatically, but consistently. If you can, you should pay the price of freedom — and not simply drift into complete dependence on the digital payment ecosystem out of sheer convenience.

My Appeal to You

Use a card when you have to. Use digital payments when they are practical. But do not give up cash voluntarily. Keep it alive, use it regularly, pay consciously in cash for small purchases, at the café, in the shop around the corner. Because cash does not disappear overnight. It disappears when we stop using it.

Conclusion: Cash Is Not an Anachronism, but a Shield

The abolition of cash is often sold as inevitable progress. I see it more as a high-risk experiment with freedom, privacy, competition, and social resilience. The deep research findings show it clearly: where cash disappears, surveillance, fee power, exclusion risks, and technical vulnerability grow.

That is why my position remains clear: Cash is not just a means of payment, but a civic right in your pocket. It is the small, everyday proof that you cannot be completely controlled, judged, and switched off.

If you take freedom seriously, then defend it where it is most tangible: at the checkout.

My closing word: Cash is the quiet guardian angel of independence. Perhaps unremarkable. Perhaps old-fashioned. But precisely in a loud, digital world, that is why it is priceless.

```

📚 Deep Research — Source Text

Dynamic Change or Digital Dystopia? A Far-Reaching Risk Analysis of the Abolition of Cash and the Global Dominance of Digital Payment Systems

1. Introduction: The Transformation of the Social Contract in the Age of Digital Payment Flows

The global transition to a cashless society represents not merely a technological upgrade of our payment infrastructure, but one of the most profound socio-economic transformations of the 21st century. Driven by rapid technological innovation, the far-reaching digitalization of global commerce, and massive regulatory efforts to curb shadow economies, global payment traffic is shifting from physical to digital media at a historically unprecedented pace. While proponents from the financial industry and government authorities often cite increased convenience, faster transaction speeds, greater tax transparency, and reduced cash-handling costs as the primary drivers of this development, a deeper analytical examination reveals structural, political, and infrastructural dangers that substantially threaten the foundations of free and democratic societies.

Money, in its most fundamental definition, is not merely an abstract medium of exchange or a neutral store of value, but a social contract deeply rooted in society between the sovereign state and its citizens. Physical cash functions in this complex structure as a so-called bearer instrument. This characteristic enables individuals to carry out transactions completely autonomously, without the mandatory involvement of a third party, without prior identity verification, and above all without leaving permanent digital traces. The gradual abolition or even the systematic marginalization of this analog anchor technology necessarily transforms the entire financial system into a purely account-based, intermediary ecosystem. In such an architecture, every transfer of value, however small, must be authorized, cryptographically verified, and permanently recorded by a centralized intermediary — whether a commercial bank, a private payment processor, or a central bank.

This paradigm shift carries far-reaching implications. The increasing digitalization of payments, which is given enormous regulatory momentum by supranational directives such as EU regulations (for example PSD2), increasingly declares traditional cash circulation an inherent risk factor for money laundering and terrorist financing. Yet this one-sided risk assessment neglects the massive disadvantages that arise for the end consumer and the independent citizen. If the trend toward card payments primarily benefits the major payment providers, the promise of technological liberation is reversed into an instrument of economic and social dependency.

This detailed research report provides an exhaustive and nuanced examination of the systemic risks that are inextricably linked to a far-reaching or complete abolition of cash. The following analysis delves into the creeping, often unnoticed loss of financial privacy made possible by algorithmic surveillance systems. It critically examines the forced integration of digital identities (e-ID) using Vietnam and Nigeria as empirical examples, where access to the financial system is coupled with biometric surveillance. A central focus also lies on the political instrumentalization of banking services — so-called de-banking — which is increasingly being used as a weapon to suppress political opponents and undesirable civil society actors.

In addition, the report analyzes the economic dimension of abolishing cash, especially the monopolistic pricing power of private payment networks such as Visa and Mastercard, which burden merchants and consumers with rising fees once cash, the fee-free substitute, has been driven out of the market. Likewise, the inherent structural fragility of purely digital infrastructures in the face of technical system failures and targeted cyberattacks is examined, since a system without an analog fallback in a crisis leads to the immediate collapse of the supply chain. Finally, using the drastic precedent of India’s demonetization in 2016, it is shown what catastrophic macroeconomic disruptions, job losses, and social trauma can arise from abrupt state intervention in cash supply.

2. The Loss of Financial Privacy and Civic Freedoms in the Digital Panopticon

Perhaps the most serious, though often most underestimated, risk of a fully cashless society lies in the establishment of a seamless and permanent surveillance infrastructure. Cash offers a unique, asymmetrical property that no conventional account-based digital means of payment has: absolute informational self-determination and complete anonymity for the parties involved. In a fully digitalized economy, by contrast, every even trivial economic interaction — from buying a coffee to donating to a political organization — mutates into a machine-readable, eternally storable data point. The renowned economist Norbert Häring aptly describes this development as a direct path to “total surveillance,” in which cashless payment dissolves the informational integrity of the individual.

2.1. Algorithmic Surveillance, Profiling, and the Concept of “Guilt by Association”

When government agencies, intelligence services, or profit-oriented private financial institutions gain unrestricted access to vast quantities of aggregated transaction data, the global financial system transforms from a mere economic infrastructure into a highly potent instrument of social control. Advanced machine learning and artificial intelligence algorithms are now easily able to build extremely complex, deeply penetrating, and often alarmingly precise personality profiles based on banal purchasing habits.

This technological capacity carries the immense danger of so-called “guilt by association.” If a completely law-abiding, non-criminal citizen purchases similar products, subscribes to identical digital services, or consumes in the same geographic patterns as police-identified criminals over a certain period, this civilian could be wrongly classified as a potential security risk through automated, opaque dragnet investigations. Mere algorithmic proximity in a multidimensional data space is enough to bring innocent people into the focus of state investigations. If state agencies were denied unregulated access to these transaction streams, innocent people could avoid being wrongly associated with criminal networks.

Moreover, the risks of data aggregation extend far into the private and commercial sectors, where algorithms decide life chances. The frequency and specific nature of purchases can be used by insurance companies, credit bureaus, and lenders to draw highly sensitive conclusions about medical conditions or dynamically recalculate default risks on loans. A citizen who, for example, regularly buys high-calorie foods, makes conspicuously frequent payments at pharmacies, or pays bills to certain medical specialist facilities could be secretly charged with much higher health or life insurance premiums through algorithmic decisions. This happens without the person ever having explicitly and informedly consented to the sharing of their health data. The financial transaction history thus becomes an unprotected electronic medical record used against the consumer.

2.2. The Legal Tension: Ethics, Human Rights, and Digital Currencies

The unstoppable mass storage of sensitive transaction data creates enormous, hardly resolvable tensions between fundamental ethical principles, international human rights standards, and the expansive goals of technology companies and governments. The universal right to privacy in the digital age is not an abstract concept, but necessarily and fully includes personal financial data. These data are subject to strict protection mechanisms against lawful and arbitrary interference, as anchored in Article 17 of the International Covenant on Civil and Political Rights (ICCPR) under international law.

The elimination of cash, without the simultaneous creation of an adequate state-guaranteed digital substitute that ensures comparable and irrevocable anonymity, therefore represents a fundamental undermining of individual freedom rights. In the current academic and monetary policy debate, there is therefore intense discussion about the design of Central Bank Digital Currencies (CBDCs). A central argument is that in a cashless society, a central bank must implement a “token-based” form of CBDC. Unlike the “account-based” variant, in which every transaction is tied to a verified identity, a token functions like a physical banknote as a digital bearer asset that can switch owners anonymously.

If nation-states or central banks instead opt for account-based digital currencies out of control motives, they are de facto violating basic international data protection principles, because identity must be disclosed to the system operator for every single financial transfer. To mitigate the problem of declining privacy, entirely new technological methods must be implemented. One approach to prevent businesses from building permanent dossiers on their customers, for example, is the use of randomized card numbers that change with each purchase and thus make it impossible to link shopping baskets to a fixed identity. Nevertheless, the basic problem remains: without cash there is no system-wide “opt-out” from data collection anymore.

3. Forced Integration: Digital ID, Biometric Capture, and Exclusion from the Banking System

The path to a cashless society rarely occurs in a regulatory vacuum. Rather, it is increasingly being tied by authoritarian as well as democratic states to the mandatory introduction of national digital identities (e-ID) and biometric databases. Where access to the financial system was once low-threshold and inclusive, it is now being repurposed into a mandatory instrument of state, unconditional data capture. A missing biometric fingerprint, an unregistered retinal scan, or an inactive digital ID leads in these systems directly to complete economic exclusion.

3.1. Vietnam’s Rigorous Biometric Reforms and the “Data-Cleansing” Shock

The Socialist Republic of Vietnam exemplifies this global trend toward the fusion of finance and state identity control with unprecedented speed and severity. As part of the Vietnamese government’s ambitiously initiated “Project 06,” launched in 2022, the construction of an all-encompassing, unified digital identity system is being pushed forward, to be fully implemented across all facets of public life by 2025, with a strategic vision through 2030. The stated intention is to create a wholly cashless society, reduce financial crime, and align the system with international standards of the OECD and the Bank for International Settlements (BIS).

The methodical implementation of these goals, however, revealed drastic consequences for the population. The State Bank of Vietnam (SBV) ordered an uncompromising “data-cleansing revolution.” As a result, more than 86 million bank accounts were deactivated, frozen, or subjected to the strictest transaction restrictions because they failed to meet the new, rigid biometric verification standards within the prescribed timeframe. As of January 1, 2025, all non-biometrically verified accounts were abruptly excluded from all online transactions, QR code scans, and digital payments. For end users, this meant that without biometric verification (such as fingerprint or facial recognition) they were effectively cut off from modern economic life. From September 2025, the final deletion of non-compliant or long-frozen accounts followed.

These massive interventions were not limited to private individuals. Under Decree No. 69/2024/ND-CP, which entered into force in July 2024, the regulatory noose is also being tightened around businesses. By July 1, 2025, all companies — explicitly including foreign organizations, representative offices, and branches — must obtain electronic identification at company level (corporate e-ID). Old digital accounts on the National Public Service Portal lose their validity abruptly after June 30, 2025. To even open such a company account, the legal representative of the business must personally have a biometric “Level-2 personal e-ID,” which must be registered either via the state VNeID platform or by appearing in person at the local police station.

Control becomes even more drastic in the mere issuance of new bank cards. Central Bank Circular 45/2024/TT-NHNN mandates from January 5, 2026 a personal face-to-face meeting between bank and customer (or company representative). At this appointment, the customer’s biometric data must be meticulously matched with the data stored on the chip of the national citizen ID card or the national electronic identification database (VNeID). A credit card can only be “activated” for electronic transactions once this biometric authentication has been successfully and unequivocally completed. The merging of bank account, everyday payment transactions, and the national biometric police database thus excludes from the economy anyone who refuses this seamless data capture.

3.2. The Nigerian Paradox: Financial Inclusion as an Instrument of Mass Exclusion

Similarly drastic, though far more chaotic due to infrastructural deficiencies, developments are currently unfolding in Nigeria, Africa’s largest economy. Under the guise of increasing security, combating fraud, and promoting financial inclusion, the Central Bank of Nigeria (CBN) tied access to bank accounts mandatorily to two digital surveillance instruments: the Bank Verification Number (BVN) and the National Identification Number (NIN). The BVN is a unique biometric identification for bank customers, introduced in 2014 to combat identity theft.

The escalation came through a CBN circular of December 1, 2023. In it, the central bank instructed that as of March 1, 2024, a so-called “Post No Debit” status (PND) would be imposed on all funded bank accounts and digital wallets that are not properly linked to a validated BVN or NIN. A “Post No Debit” status is a draconian measure: it blocks the account completely for withdrawals, transfers, or any debits and effectively freezes customer funds indefinitely.

The demographic and humanitarian consequences of this deadline were fatal. An estimated 70 million bank customers immediately risked losing access to their essential accounts overnight. Especially dramatic was the instruction that this linkage requirement now also applied mandatorily to so-called “Tier-1 accounts.” These basic accounts (with a deposit limit of N50,000 and a maximum balance of N300,000) were originally created specifically to be opened with minimal hurdles — often just via USSD code on a mobile phone — in order to integrate the poorest of the poor into the financial system. Suddenly, exactly these people were criminalized and excluded if they could not present biometric identification. Banks were warned that non-compliance would be punished with drastic regulatory fines, as illustrated by Guaranty Trust Bank, which was fined 128.6 million naira in 2023 for regulatory shortcomings. This forced institutions into preemptive, rigorous action against their own customers.

Implementation exposed the brutal reality of a coerced digital system in a developing country. A glaring infrastructural bottleneck emerged. Around 300 of Nigeria’s 774 local government areas (LGAs) have no bank branches at all, making it physically impossible for millions of rural residents to complete BVN registration. Compounding the issue, the National Identity Management Commission (NIMC) lacked the capacity to close the estimated gap of 100 million missing NINs within the short deadline. A chronically unreliable power grid — while 91.4% of the urban population has electricity, only 30.4% do in rural areas — and poor telecommunications networks prevented countless citizens from even charging their phones to complete the digital validation processes.

The consequences were panic and chaos. Customers besieged the few urban bank branches as early as 8:00 a.m. in desperation, while confusing automated bank texts also frightened customers who had already registered. Industry representatives, such as the president of the Association of Mobile Money and Bank Agents in Nigeria, spoke of massive economic trauma for a population already suffering under adverse economic conditions. The result of this field experiment is paradoxical: although the government aimed for a 95% financial inclusion rate by 2024, the forced digital ID mandate in reality led to economic disenfranchisement. Rural residents remain heavily disadvantaged (37% financial exclusion in rural areas compared with 17% in cities). Instead of making life easier, the system excluded millions from society and proved that digital identities combined with account coercion constitute a dangerous instrument of exclusion.

4. The Political Weapon of the Financial System: “De-Banking” and the Danger to the Opposition

When physical cash disappears from society and access to electronic means of payment becomes the unavoidable basic prerequisite for the most elementary participation in social life, the financial system transforms into a highly political actor. The withdrawal of this access becomes a fatal and precise weapon. This phenomenon, known in specialist circles as “de-banking,” describes the sudden, often automated closure or freezing of an individual’s or organization’s bank accounts, usually without transparent justification, without warning, and without realistic legal recourse. In recent years, de-banking has rapidly developed into a globally used instrument of political and social repression, applied in both dictatorships and Western democracies. It functions as a form of economic exile that drives small businesses into bankruptcy, strips non-profit organizations of funding, and forces individuals into the hands of predatory payday lenders just to pay basic bills.

4.1. The Paralysis of Political Dissidents in Authoritarian Systems

In authoritarian systems, control over the financial system is the most effective, quietest means of completely neutralizing political opposition. The Russian state demonstrated this in drastic fashion in its actions against the now-deceased Kremlin critic Alexei Navalny. In 2020, Navalny’s personal bank accounts, the accounts of his family members (parents, wife, children), and the accounts of the head of his Anti-Corruption Foundation (FBK), Ivan Zhdanov, were systematically frozen by Russian authorities. To suffocate any financial freedom of movement, absurd, artificially generated negative balances of 75.5 million rubles (at the time over 1.1 million U.S. dollars) were displayed to the affected individuals in their online banking portals. This accounting trick completely paralyzed their ability to act and their day-to-day livelihood, since any incoming funds would have been immediately swallowed by this fictitious mountain of debt.

The pretexts for these coordinated actions were legally engineered. Often they were based on civil defamation lawsuits by Kremlin-linked oligarchs or catering companies whose corruption had been exposed by Navalny’s team. In addition, raids were carried out by investigators and proceedings were initiated for alleged “money laundering” of donations in the billions. Navalny’s spokeswoman, Kira Yarmysh, also reported that even apartments were seized, so they could neither be sold, mortgaged, nor rented out. Navalny himself described this as a direct attempt by President Vladimir Putin to crush the work of the FBK and discredit him publicly. Without cash as an unmonitored fallback, such a coordinated state intervention inevitably leads to the civic and economic death of those affected.

A similarly restrictive approach emerged in the financial center of Hong Kong. In the wake of the repressive enforcement of the National Security Law imposed by Beijing in 2020, pro-democracy activists increasingly came under the banks’ scrutiny. In 2023, for example, the global major bank HSBC froze the accounts of the pro-democracy activist group “League of Social Democrats” without providing comprehensible reasons. Party chair Chan Po-ying, who had previously been arrested during protests, complained at a demonstration in front of the lion statues at HSBC headquarters that the “cancellation of bank accounts is soft political persecution.” Since the party was no longer allowed under restrictive laws to collect donations physically in the street, it was existentially dependent on digital transfers; the account freeze stopped the political organization’s survival at its roots.

The reach of this de-banking extends even beyond national borders to political refugees. Pro-democracy politicians who fled into exile in Australia or the United Kingdom — such as former lawmaker Ted Hui — were denied access to their legally acquired pension funds (worth in some cases over HK$600,000) by Western financial institutions (such as Canada’s Manulife). The justification given by the financial institutions was that the Hong Kong police had issued arrest warrants against the activists for violations of the National Security Law and that their accounts were “under investigation.” The activists criticized the hypocrisy of these institutions, which on the one hand profess allegiance to international human rights standards but on the other act as compliant enforcers of authoritarian laws and drive exiles into financial hardship.

4.2. The Infiltration of De-Banking into Western Democracies

The dangerous weapon of de-banking is by no means limited to autocracies; it is increasingly infiltrating the structures of Western democracies, often disguised under the cloak of compliance, risk aversion, and reputational protection.

A striking example occurred in Canada in February 2022 during the protests of independent truck drivers (known as the “Freedom Convoy”), who demonstrated against government COVID-19 vaccine mandates. In an unprecedented coordinated action, major Canadian commercial banks such as RBC (Royal Bank of Canada) and CIBC froze the private and business accounts of numerous protest participants and organizers. Bank representatives officially justified this massive encroachment on fundamental rights by claiming that freezing the accounts was a necessary response to “potential fraud and money laundering.” De facto, however, the measure clearly served as an instrument to suppress the protest movement in cooperation with the government by simply cutting off the demonstrators’ financial lifelines — for fuel, food, and logistics. Because the financial sector is a highly regulated industry in which banks face enormous regulatory pressure when suspicions arise, once individuals are “de-banked” they have little chance of opening an account at another institution. If you are banned from Twitter, you can still speak on other platforms; but if you are excluded from banking services, you have nowhere to go, which poses a fundamental threat to democratic participation.

In the United Kingdom, the case of former politician and Brexit supporter Nigel Farage sparked a national scandal in the summer of 2023 that exposed the inner workings of reputational de-banking. The prestigious private bank Coutts (a subsidiary of the NatWest Group) abruptly closed Farage’s account. While the bank initially claimed that Farage no longer met the institution’s financial “elite criteria,” a Subject Access Request forced by Farage revealed the real motivation. Internal documents from the bank’s reputational risk committee showed that the account was closed primarily because Farage’s political views allegedly did not align with the bank’s “values” and inclusion philosophy.

The resulting media and political uproar led to a far-reaching investigation. An independent report by the renowned law firm Travers Smith uncovered serious failings by the bank in its handling of Farage. Although the report formally classified the closure as “lawful” based on internal bank policy, it criticized major deficiencies in decision-making, communication, and the handling of confidential customer data by management. This scandal ultimately forced both Coutts’ CEO and the chief executive of parent company NatWest, Dame Alison Rose, into humiliating resignations and temporarily wiped more than £1 billion from the bank’s market value. The British financial regulator FCA (Financial Conduct Authority) was compelled to launch investigations and request reports from institutions, and it was shockingly revealed that the banks’ records on account closures were chaotic, incomplete, and the reasons extremely vague. In 2022 alone, nearly 350,000 accounts were closed in the United Kingdom — an eightfold increase within five years.

In the United States as well, major banks are coming under increasing political pressure as they use their market power to enforce moral guidelines. The Office of the Comptroller of the Currency (OCC), in a preliminary report, expressed concerns that major U.S. banks (including JPMorgan Chase, Bank of America, Citi, and Wells Fargo) made inappropriate distinctions among customers between 2020 and 2025 due to internal ESG (Environmental, Social, and Governance) policies. Institutions with ties to politically polarizing industries such as oil and gas, firearms, private prisons, or certain political action committees (PACs) were denied access or made unable to obtain it through endless review loops. Conservative activists and organizations such as Alliance Defending Freedom (ADF) complain of being systematically targeted by campaigns from activist groups (such as the Southern Poverty Law Center) that pressure financial institutions to terminate these organizations’ accounts. Payment processors such as WePay (a JPMorgan subsidiary) also terminated contracts for conservative events under the vague accusation of “promoting hate,” illustrating the enormous ideological power of private payment intermediaries.

The table below synthesizes the most prominent international precedents and illustrates the mechanisms and destructive consequences of political de-banking.

Incident & GeographyActor (Financial Institution / Authority)Affected Organization / IndividualOfficial Justification for De-BankingResulting Impact on Those AffectedRussia (2019-2020)Russian investigative authorities

Alexei Navalny, relatives, Anti-Corruption Foundation (FBK)

Alleged fraud, money laundering, lawsuits by oligarchs

Freezing of all funds, generation of absurd negative balances (-75.5 million rubles) to paralyze, seizure of real estate.

Hong Kong (from 2020)

HSBC, Manulife (Canada)

League of Social Democrats, exiled activists (Ted Hui)

Suspicion of violations of the National Security Law

Operational loss of the party’s existence (donation intake blocked), withholding of legal pension funds worth millions from exiles.

Canada (Feb. 2022)

RBC, CIBC, Canadian government

“Freedom Convoy” trucker protests & sympathizers

Prevention of “potential fraud and money laundering”

Suppression of legitimate political protest by starving demonstrators and blocking logistical financing.

UK (2023)

Coutts private bank, NatWest Group

Nigel Farage (former UKIP/Brexit party leader)

Political views did not align with the bank’s “corporate values”

Reputational damage to the bank, resignation of the CEO, exposure of serious governance failings through the Travers Smith report.

USA (2020-2025)

JPMorgan Chase, Bank of America, Citi, WePay

Gun manufacturers, private prisons, conservative PACs, ADF

Violation of ESG policies, alleged promotion of “hate”

Withdrawal of basic payment services from legal but socially controversial industries and political committees.

5. Economic Monopolization: The Fee Explosion in a World Without a Cash Alternative

Another major macroeconomic risk of removing the cash alternative is the unchecked, absolute monopolistic pricing power of private payment providers. From a macroeconomic perspective, cash operates as an essential public good. It functions not only as legal tender, but above all as a natural anchor and permanent brake on prices in the payment market. As long as consumers and merchants have the option of switching to fee-free physical cash, private payment providers are forced to keep their fees competitive. But if this analog fallback disappears, merchants — and consequently consumers through price markups — are left defenseless against the fee structures and return expectations of the dominant publicly traded payment networks. Worldwide, the costs of payment fees amount to an unimaginable sum of around 2 trillion U.S. dollars annually.

5.1. The Market Power of the Duopoly: Visa, Mastercard, and the Illusion of Competition

The global architecture for digital card payments is largely dominated by an overpowering duopoly: Visa and Mastercard. The theoretical assumption that digital scale effects should drive the costs of electronic payments toward zero over time is consistently disproved by the pricing practices of this duopoly.

A far-reaching market review by the UK Payment Systems Regulator (PSR), whose interim report was published in May 2024, provides empirical evidence. The authority found that Visa and Mastercard in the United Kingdom face “ineffective competitive constraints” in providing network and processing services to merchants and acquirers (merchant banks). In recent years, the regulator observed continuous and significant fee increases for which no plausible justification could be found on the basis of rising operating costs, measurable quality improvements, or increased innovation efforts.

This market power became especially blatant in cross-border transactions after Brexit. The PSR’s investigations showed that Visa and Mastercard massively raised the so-called interchange fees for online transactions between the European Union and the United Kingdom in the period 2021 to 2022: to 1.15% of the transaction value for debit cards and to a hefty 1.5% for credit cards. Chris Hemsley, then Managing Director of the PSR, stated unambiguously that these fees were “likely too high” and that the market was “not working well.”

For local retail, this problem is exacerbated by the structural opacity of fee models. As the Association of Convenience Stores (ACS), which represents nearly 50,000 British retailers, explained in a submission to the PSR, small and medium-sized merchants are often blind to the true costs. Through the widespread “blended pricing model,” merchants receive only lump-sum invoices from their payment processors. The highly complex, consisting of hundreds of individual tariff components, mandatory or behavior-based fees of the card networks are deliberately obscured in these bills. Even in the more transparent “Interchange++” model, often only the interchange fee is shown, while the actual network scheme fees remain hidden. This lack of transparency makes it impossible for retailers to push back against specific fee increases. The inevitable consequence: the merchant must factor these ever-rising overhead costs into margin calculations and pass them on to the entire population through higher consumer prices.

Even in markets where political efforts exist to limit card fees through comparisons or caps, the supremacy of the networks becomes evident. In the United States, a long-awaited settlement on reducing credit card fees was recently reached. Yet it merely proposed to lower the average “swipe fee” marginally from 2.35% to 2.25%. Retail representatives reacted with outrage. Sean Kennedy, spokesperson for the National Restaurant Association, called it remarkable that a temporary reduction of a ridiculous 10 basis points — barely more than the increase of the previous year — should be seen as fair compensation for allowing a “credit card duopoly to maintain its price cartel for another eight years.” When the corrective force of cash is absent, payment traffic turns into an inelastic compulsory levy on all commerce.

5.2. The Swedish Warning: When the Point of No Return Has Been Crossed

Sweden — the global pioneer of the cashless society — demonstrates how dramatic dependence on private payment providers becomes once cash truly disappears from the economic cycle. In Sweden, cash transactions have already fallen to a vanishingly small share of under 2% of the total value of all payments, while credit and debit cards and the ubiquitous mobile payment app “Swish” dominate the market.

Academic studies estimate the so-called “point of no return” — the point at which cash infrastructure functionally collapses — at a transaction share of about 7%. Once usage falls below this critical threshold, the fixed costs of cash handling (such as armored cash transporters, secure vaults, and sorting machines) simply become uneconomical. Sweden has long since crossed that threshold. Astonishingly, around 900 of Sweden’s 1,600 bank branches no longer handle cash, do not accept cash deposits, and thousands of bank ATMs in rural areas have been removed without replacement. Cash in circulation in Sweden has fallen from 106 billion kronor in 2009 to around 80 billion. Relative to GDP, the value of Swedish cash transactions stands at only 1%.

This transformation was facilitated by specific Swedish contract law. Unlike in countries with strong consumer protection, contract law in Sweden (freedom of contract) takes precedence over banking law. This allows retailers, cafés, and even hospitals to refuse legal tender, as long as they put up a simple “No cash accepted” sign before the contract is concluded.

While this development appears superficially smooth and has contributed to an e-commerce boom and a decline in violent bank robberies, Swedish merchants are now trapped in the fee pit. They are completely at the mercy of payment providers’ price dictates, because they can no longer ask customers to “just pay in cash” when card fees rise. A far-reaching report by Boston Consulting Group (BCG) identifies a bracing paradox in this context: although digital solutions can stimulate macroeconomic growth, the enormous savings for merchants (through the elimination of labor-intensive cash handling) are often completely eaten up — or even surpassed — by higher, unregulated card fees that are indirectly borne by customers as well. When payments become a proprietary walled garden of private actors, society as a whole pays an enormous structural rent to a handful of monopolists.

6. Infrastructure Fragility: Technical Errors, System Outages, and the Age of Cyberattacks

The unconditional transition to a purely digital payment architecture transforms what was once an extremely decentralized, physical system with very high fault tolerance into a tightly coupled, hyper-complex electronic network. Cash is resistant to failure: a power outage, a faulty router, or a server crash in a data center does not stop two people from exchanging a banknote. Digital systems, by contrast, are necessarily dependent on an uninterrupted chain of authentications, data connections, and energy supply. Without the analog fallback of physical cash, any technological disruption — whether intrinsic through software bugs (system outage) or extrinsic through malicious actors (hacker attack) — inevitably leads to the immediate, nationwide collapse of the civilian supply chain.

6.1. Catastrophic System Outages and the Illusion of 100% Availability

Historical precedents from recent years impressively demonstrate the enormous dangers and real fragility of IT infrastructure failures in core areas of finance.

In June 2018, the European continent experienced an unprecedented collapse of the Visa network. On a busy Friday afternoon, the central authorization system for Visa Europe card payments collapsed. The cause was not a hostile cyberattack, but simply a serious systemic hardware failure. The effects were immediate and dramatic: millions of people in the United Kingdom and across Europe suddenly stood at supermarket checkouts, gas stations, restaurants, and international airports with no way to pay for their goods. Social order faltered, merchants had to turn customers away, and unprecedented chaos ensued as many consumers had long since stopped carrying cash because of the trend toward cards. The extent of the disruption was so critical to trust in the financial system that the Bank of England (BoE) intervened and pressed Visa to strictly implement the recommendations of an independent investigation by PricewaterhouseCoopers (PwC) under supervision. Visa’s global CEO had to apologize publicly and admit that the company had “clearly failed” its core goal of reliable payment processing 24 hours a day, 365 days a year.

Even more devastating for the individual consumer are faulty system migrations at the account-holding institutions themselves. In April 2018, the British TSB Bank orchestrated the highly complex migration of millions of customer records from the platform of its former parent company Lloyds to a new IT platform belonging to its new owner Sabadell. The migration became a fiasco. The new platform immediately exhibited fatal errors: digital online banking, branch technology, and the entire internal payment system collapsed under the strain. Customers could neither transfer money nor pay bills. Worse still: basic data integrity was severely compromised, so that after logging in, customers suddenly could see transactions, balances, and highly sensitive data belonging entirely to strangers.

The resulting surge of angry customers brought the bank’s phone and support systems completely to a standstill. TSB Bank remained in an operational state of emergency until December 2018 — almost nine months — in which normal business operations were impossible. The financial and regulatory consequences for the bank were immense: an independent investigation report by the law firm Slaughter and May uncovered massive planning errors. TSB had to pay more than £32 million in direct compensation for the more than 225,000 customer complaints received. Ultimately, the bank was fined a draconian total of £48.65 million by the UK regulators, the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) (already including a 30% discount for cooperation). For customers, however, the incident painfully demonstrated that trusting digital balances is literally worth nothing in an emergency when the underlying database fails.

This operational fragility is further amplified by broader macroeconomic banking crises. The year 2023 marked some of the largest, fastest, and most devastating bank failures in U.S. history, with the rapid collapse of giants such as Silicon Valley Bank, Signature Bank, and First Republic Bank. In a fully cashless world, the temporary collapse of an account-holding institution triggered by a bank run or mismanagement means affected citizens are instantly and absolutely cut off from any form of liquidity until government deposit insurance funds painstakingly take effect.

Moreover, massive interconnection creates entirely new dependencies on third parties. A faulty software update by cybersecurity firm CrowdStrike in July 2024 caused a global IT outage that brought not only airlines and media companies but banks and card issuers worldwide to their knees temporarily. Even though the core networks of Visa and Mastercard reported that their systems were “working smoothly,” countless consumers could not make payments because the systems of card-issuing banks and merchant point-of-sale systems were wrecked by the faulty update. This chain of dependencies proves that the financial sovereignty of a nation in a cashless world is extremely endangered.

6.2. The Invisible Threat: Hacker Attacks, Data Leaks, and Cybercrime

In addition to unintentional technical failures, the massive centralization of highly sensitive financial data forms an irresistible and extremely lucrative target for organized cybercrime and state-backed hacker collectives. Since hackers always select targets according to two main criteria — maximum damage and maximum financial profit — the financial sector is the most attacked ecosystem in the world, right after (or on par with) healthcare.

A particularly alarming example of the perfection of modern cyberattacks occurred at the U.S. payment processor Slim CD. The company processes credit card payments for countless merchants in the United States and Canada. As the company admitted, professional hackers managed to operate unnoticed inside the payment provider’s internal network for almost ten months (from August 2023 to June 15, 2024). In a tiny, decisive window between June 14 and 15, 2024, the criminals were finally able to exfiltrate the highly sensitive data of nearly 1.7 million individuals. The stolen records included full names, physical addresses, full 16-digit credit card numbers, and expiration dates. That such a massive, long-lasting breach at a “payment processing giant” went undetected by security systems for almost a year raises fundamental questions about security architectures and reveals that many companies cut corners on robust data security to save costs. Although the CVV verification numbers were not taken, the data package is more than sufficient for various forms of identity theft and targeted fraud.

Another enormously serious event illustrates the danger of internal misconfigurations that lead to massive data leaks. In May 2019, an incredible 885 million financial and personal records of First American Financial Corporation, a giant in U.S. real estate finance, were left completely unprotected on the internet. In this case, the cause was not even a sophisticated hacker attack with malware, but a banal “business logic flaw.” A design error on the company website meant that web links to highly sensitive financial documents (bank statements, mortgage contracts, social security numbers) were simply not protected by a basic authentication check (password or token); anyone who slightly altered the link parameter could view millions of other people’s files.

This systemic vulnerability runs through the entire industry. Further security incidents in recent times, such as at the platform Finexio (loss of $800,000 due to compromised internal workflows in January 2025), Payoneer (targeted exploitation of API vulnerabilities in February 2025), or at Checkout.com, demonstrate the sheer range of attack vectors.

The table below aggregates the most serious system outages and hacker attacks of recent history. It structurally illustrates that these incidents are not isolated anomalies, but a troubling systemic risk pattern in which millions of people have been massively harmed by hardware, software, and security vulnerabilities.

Date, Affected Parties, Institution, Incident Category, Documented Impacts & Causes

April 2018 TSB Bank (UK)Catastrophic system outage

Failed IT migration led to the complete outage of online banking and payments for 1.9 million customers. Data integrity compromised (viewing other people’s accounts). Bank was paralyzed for months, 225,000 complaints.

June 2018 Visa Europe system outage (hardware)

A serious hardware failure caused a Europe-wide outage of card authorization systems. Millions of consumers could not pay in supermarkets and at gas stations.

May 2019 First American Financial Corp. data leak (business logic flaw)

A flawed web design without authentication protection made 885 million highly sensitive financial and real estate records openly accessible to anyone on the internet.

July 2024 Global banks (via CrowdStrike) system outage (software update)

A faulty update from a third-party security software provider paralyzed IT systems at banks and merchant terminals worldwide, making card payments impossible.

Aug 2023 - Jun 2024 Slim CD (payment gateway) hacker attack (data theft)

Hackers infiltrated the network unnoticed for 10 months. Exfiltration of 1.7 million customer records, including names, addresses, and full credit card numbers.

7. Macroeconomic Shock Therapy as a Lesson: India’s “Demonetization” (2016)

In order to fully understand the devastating socio-economic implications and sheer destructive potential of abrupt state-led cash abolition, India serves as perhaps the most important historical lesson in recent financial history. In November 2016, the Indian government under Prime Minister Narendra Modi carried out an unprecedented, risky monetary intervention. Overnight, in true “shock therapy” that caught the country completely unprepared, the government declared the existing 500- and 1,000-rupee banknotes invalid and stripped them of legal tender status.

Because these specific notes together accounted for a massive 86% of the country’s total circulating cash, and the Indian economy functioned with almost 90% dependence on cash, this “demonetization” literally cut the oxygen supply to the economic cycle from one second to the next. The measure plunged the world’s largest democracy into unprecedented social and economic chaos.

7.1. The Failure of Anti-Corruption Goals and Economic Paralysis

The officially declared main goal and the grand political narrative behind this draconian reform was to wipe out the flourishing black market, endemic corruption, terror financing, and widespread tax evasion with a single bold strike. According to government statements, only about 1% of Indians paid income tax in 2013. After the announcement, the population was given a strict deadline until December 30, 2016, to deposit or exchange the now-invalid banknotes at banks.

However, economic analyses and official data quickly showed that the “demonetization” failed grandly as a precise tool against corruption: contrary to the government’s hopes that illegal black money would simply vanish for fear of discovery, an incredible 97% of the invalidated cash (nearly 15 trillion rupees out of 15.4 trillion) was, according to central bank reports, successfully returned to the legal banking system. Shadow-economy actors found sophisticated methods of laundering money — through straw men, fake invoices, or advance tax payments (for example, tax revenue in the city of Hyderabad rose by 1.6 billion rupees in cash over four days) — to save their holdings. Moreover, a conceptual error became clear: truly accumulated black wealth was no longer hidden en masse as physical paper money under mattresses (surveys showed that only about 6% of illicit wealth was held in cash), but was profitably tied up in asset classes such as real estate, gold, jewelry, or company shares.

While black money was saved, the collateral damage to ordinary people and the real economy was apocalyptic. Since Indian banks and printing facilities were unable for months to produce and distribute enough new banknotes (which, ironically, had a different physical size and therefore required months of costly recalibration of hundreds of thousands of ATMs), liquidity dried up nationwide. Even the Indian Air Force had to be deployed to fly the few new notes across the country. Banks were forced to impose draconian withdrawal limits (initially a maximum of 2,500 rupees per day and 24,000 rupees per week), causing millions of desperate citizens to queue for hours daily in front of empty ATMs in the hope of withdrawing their own money.

This artificially created liquidity shock hit the enormous informal sector hardest. This sector, which accounts for 45% of India’s economic output and employs an incredible 94% of the working population, traditionally operates almost exclusively on a cash basis and was completely paralyzed. The renowned Centre for Monitoring Indian Economy (CMIE) estimated that the employment rate fell drastically and the working population shrank from 439.7 million (2016-17) to 426.1 million (2017-18); an estimated 1.5 million jobs were simply destroyed as a result of the cash shortage. Consumption also collapsed in real time: sales of fast-moving consumer goods (FMCG) at companies like Nestlé fell sharply. In the automotive sector, two-wheeler (scooter) sales in December 2016 dropped by 22% — the steepest decline since 1997 — and growth in tractor sales for agriculture slowed from 28% to 18%. The economy was artificially pushed into recession (researchers estimate economic activity fell by at least 3 percentage points in the following months).

7.2. The Real Purpose: The Forced Digitalization of Society

If the primary goal of combating corruption therefore largely failed, the measure nonetheless served as a brutal, highly effective catalyst for the forced dictatorship of digital payments in India. With the complete absence of physical cash for weeks, mobile payment systems experienced explosive, panic-driven demand. Market leaders such as the e-wallet provider Paytm saw absurd increases in usage within a very short time: app traffic rose by 435%, and the value of processed transactions jumped by 250%. Credit and debit card use at point-of-sale systems also exploded.

The Modi government aggressively used this momentum to push its own technological innovations of Digital Public Infrastructure (DPI) into the market. It forced the use of the state-run BHIM app, which enabled electronic real-time transfers between bank accounts based on the biometric, 12-digit national Aadhaar ID. This push was accompanied by hard regulatory coercion: acceptance of digital payments was simply made mandatory for strategic nodes such as gas stations, hospitals, and universities, while cash transactions above US$4,500 were completely banned. To force the shift, authorities also abruptly eliminated taxes on point-of-sale devices and biometric fingerprint readers.

India’s radical experiment brutally exposes the cruel ambivalence of such top-down “reforms” toward a cashless society: they mercilessly destroy the fragile economic livelihoods of millions of informal workers and wipe out jobs, while at the same time, under the guise of modernization, using state power to force the infrastructure of all-encompassing, seamlessly monitored digital payments.

8. Synthesis and Conclusion: The Need for Digital Alternatives and the Preservation of Sovereignty

The ongoing and politically desired displacement competition against physical cash is far more than a convenient technological evolution of economic transaction. It is the creeping but unstoppable transition from a decentralized, freedom-oriented, data-sparing, and extremely fault-tolerant exchange system to a panoptic, monopolistically dominated, and structurally highly volatile digital control architecture.

The comprehensive analysis in this research report shows impressively that a far-reaching or even complete abolition of cash destroys the fundamental civil right to anonymity. Through the unavoidable loss of informational privacy, citizens become economically transparent and, through AI algorithms in the sense of a new surveillance capitalism, calculable, stigmatizable, and sanctionable. The forced introduction of digital IDs in countries like Vietnam and Nigeria empirically demonstrates that coupling financial services to biometric surveillance brutally excludes from the economic cycle all those who are critical of such registration or who simply lack the physical and technological infrastructure — as in Nigeria’s rural population — to participate in this system.

Moreover, the unconditional compulsion toward digital transactions establishes highly dangerous, quiet instruments of political repression. As the various cases in Russia, subjugated Hong Kong, democratic Canada, and the United Kingdom demonstrate, the phenomenon of “de-banking” has matured into a precise and lethal weapon. With it, states or morally motivated private financial institutions can economically destroy dissidents, unwelcome protesters, and politically undesirable actors at the push of a button, effectively excluding them from civil society and democratic discourse.

Economically, the displacement of the fee-free public good “cash” primarily benefits an uncontrolled, profit-driven oligopoly of private card issuers and payment processors. Companies like Visa and Mastercard use this monopoly position to impose their lucrative fee models unregulated on retailers and thus ultimately on the buying public as an invisible tax in the absence of cash. Last but not least, ongoing massive hacker attacks on payment processors, catastrophic IT migration disasters at major banks, and simple hardware outages reveal that a purely digital financial architecture is inherently extremely vulnerable to “single points of failure.” The scale of this vulnerability can be fatal in a crisis and paralyze entire economies.

If free societies and democracies continue to pursue the path toward a predominantly digital economic order, the underlying infrastructure must be conceived as a public, common-good-oriented asset. The development of token-based central bank digital currencies (CBDCs) that are technologically designed and legally protected so as to preserve the irrevocable anonymity of cash and also function absolutely fail-safe offline is indispensable to protect citizens’ rights. Without the continued, guaranteed protection of physical cash as an eternal fallback, or the creation of absolutely privacy-compliant, decentralized alternatives, the shining utopia of convenient, frictionless payments threatens to turn into an unprecedented, all-encompassing digital dystopia in which access to money is a privilege that can be withdrawn at any time.

Cash is the Real Thing — Abolishing Cash Carries Risks - Dr. Datenschutz

Cash is the Real Thing — Abolishing Cash Carries Risks - Dr. Datenschutz

Navigating the Transition: Impacts, Challenges and Future Prospects of a Cashless Society

Wird in einem neuen Fenster geöffnet

How important is cash? | Verbraucherzentrale NRW

Wird in einem neuen Fenster geöffnet

Wird in einem neuen Fenster geöffnet

Cashless Society: Managing Privacy and Security in the Technological Age - ResearchGate

Wird in einem neuen Fenster geöffnet

Wird in einem neuen Fenster geöffnet

Factors That Determine the Adoption of Nigeria's Central Bank Digital Currency (E-Naira)

Wird in einem neuen Fenster geöffnet

The State Bank of Vietnam (SBV) has deactivated over 86 million ...

Wird in einem neuen Fenster geöffnet

Vietnam Requires Corporate e-ID from July 1, 2025 - Vietnam Briefing

Wird in einem neuen Fenster geöffnet

Navigating Vietnam's e-ID requirements for business administration - Allen & Gledhill

Wird in einem neuen Fenster geöffnet

Vietnam adopts mandatory biometric authentication for new bank cards

Wird in einem neuen Fenster geöffnet

Vietnam has big digitalization and biometrics ambitions for 2026

Wird in einem neuen Fenster geöffnet

Wird in einem neuen Fenster geöffnet

How to Turn the CBN's NIN/BVN Policy into Your Bank's Strategic Advantage - Seamfix

Wird in einem neuen Fenster geöffnet

NIN linkage: Banks may block 70 million accounts

Wird in einem neuen Fenster geöffnet

Banks: No going back on NIN/BVN linkage to account deadline - The Nation Newspaper

Wird in einem neuen Fenster geöffnet

Sustainable financial inclusion in Nigeria: a need to go beyond access to impact

Wird in einem neuen Fenster geöffnet

Nigeria: Freedom on the Net 2024 Country Report

Wird in einem neuen Fenster geöffnet

Formal financial inclusion in Nigeria soars to 64%, driven by non-banking channels” – Report - A2F

Wird in einem neuen Fenster geöffnet

How De-Banking Became a Conservative Rallying Cry - New Lines Magazine

Wird in einem neuen Fenster geöffnet

Wird in einem neuen Fenster geöffnet

Kremlin critic Navalny's 'bank accounts frozen, apartment seized' | News | Al Jazeera

Wird in einem neuen Fenster geöffnet

Accounts of Russian Opposition Politician Navalny, Associate Frozen - VOA

Wird in einem neuen Fenster geöffnet

Russia Freezes Bank Accounts Linked to Opposition Politician Navalny Following Raids

Wird in einem neuen Fenster geöffnet

Navalny Says Kremlin Has Frozen His Bank Accounts - Courthouse News Service

Wird in einem neuen Fenster geöffnet

Hong Kong opposition party activists protest account closures at HSBC head office

Wird in einem neuen Fenster geöffnet

Exiled pro-democracy Hong Kong activists blocked from accessing pensions - The Guardian

Wird in einem neuen Fenster geöffnet

Hong Kong cops told banks to block politician's accounts - YouTube

Wird in einem neuen Fenster geöffnet

De-banked: The threat of cancel culture in the financial industry ...

Wird in einem neuen Fenster geöffnet

The Conduct Chronicles: "Lessons from the Farage Bank Account" - Global Relay

Wird in einem neuen Fenster geöffnet

Read the full NatWest report on Nigel Farage's Coutts account row - Evening Standard

Wird in einem neuen Fenster geöffnet

Key findings from Phase 1 of Travers Smith review - NatWest Group

Wird in einem neuen Fenster geöffnet

No evidence Coutts closed accounts due to political views, report says - The Guardian

Wird in einem neuen Fenster geöffnet

OCC cites 9 big banks' 'inappropriate' debanking actions - Banking Dive

Wird in einem neuen Fenster geöffnet

De-banking: Cancel Culture's Newest Threat - Alliance Defending Freedom

Wird in einem neuen Fenster geöffnet

The Good, the Bad, and the Ugly Sides of a Cashless Society

Wird in einem neuen Fenster geöffnet

electronicpaymentsinternational.com

UK payments regulator accuses Mastercard, Visa of restricting competition

Wird in einem neuen Fenster geöffnet

Visa, Mastercard and Revolut Lose UK Battle Over Interchange Fees | PYMNTS.com

Wird in einem neuen Fenster geöffnet

Market review of card scheme and processing fees - Payment Systems Regulator (PSR)

Wird in einem neuen Fenster geöffnet

8 pros, cons of Visa-Mastercard pact | Payments Dive

Wird in einem neuen Fenster geöffnet

The Swedish payments market is almost entirely digital | Sveriges Riksbank - Riksbanken

Wird in einem neuen Fenster geöffnet

Sweden's cashless revolution: Is this the end of paper money? - SBS Software

Wird in einem neuen Fenster geöffnet

Cashless Societies: Which Countries Are Making The Switch? - Corepay

Wird in einem neuen Fenster geöffnet

Sweden leads the race to become cashless society | Banking - The Guardian

Wird in einem neuen Fenster geöffnet

Going Cashless: What Can We Learn from Sweden's Experience? - Knowledge at Wharton

Wird in einem neuen Fenster geöffnet

Why Sweden's cashless society is no longer a utopia | World Economic Forum

Wird in einem neuen Fenster geöffnet

Do we have the right to pay in cash? | Sveriges Riksbank - Riksbanken

Wird in einem neuen Fenster geöffnet

FALQs: Cashless Sweden | In Custodia Legis - Library of Congress Blogs

Wird in einem neuen Fenster geöffnet

How Cashless Payments Help Economies Grow - Boston Consulting Group

Wird in einem neuen Fenster geöffnet

What Going Cashless Means for High-Risk Merchant Accounts | Corepay

Wird in einem neuen Fenster geöffnet

Bank of England announces supervisory action over Visa Europe's June 2018 partial outage incident

Wird in einem neuen Fenster geöffnet

Visa outage: payment chaos after card network crashes – as it happened - The Guardian

Wird in einem neuen Fenster geöffnet

Visa card payments system returns to full capacity after crash - The Guardian

Wird in einem neuen Fenster geöffnet

Letter from Visa regarding service disruption, 15 June 2018 - UK Parliament

Wird in einem neuen Fenster geöffnet

Resilience failures: Why was TSB Bank fined and what can we learn from it? - Protecht

Wird in einem neuen Fenster geöffnet

TSB Board publishes independent review of 2018 IT Migration

Wird in einem neuen Fenster geöffnet

Wird in einem neuen Fenster geöffnet

TSB fined £48.65m for operational resilience failings | Bank of England

Wird in einem neuen Fenster geöffnet

After 2023 Bank Failures—Here’s Our Roadmap for Improving Bank Oversight | U.S. GAO

Wird in einem neuen Fenster geöffnet

15 most recent bank failures | American Banker

Wird in einem neuen Fenster geöffnet

List Of Failed Banks: 2009-2026 | Bankrate

Wird in einem neuen Fenster geöffnet

Bank Failures in Brief – Summary - FDIC

Wird in einem neuen Fenster geöffnet

2025 in Brief - Bank Failures | FDIC.gov

Wird in einem neuen Fenster geöffnet

Visa, Mastercard say CrowdStrike didn’t impact networks | Payments Dive

Wird in einem neuen Fenster geöffnet

Understanding Service Disruptions at X, Workday & Mastercard - YouTube

Wird in einem neuen Fenster geöffnet

Global Mastercard Payment Outages Lead To Consumer Complaints - PYMNTS.com

Wird in einem neuen Fenster geöffnet

Status Update on Outages and Issues - Mastercard

Wird in einem neuen Fenster geöffnet

14 Biggest Data Breaches in Finance - UpGuard

Wird in einem neuen Fenster geöffnet

Payment Gateway Reveals Hack Affecting 1.7 Million Cards - PaymentsJournal

Wird in einem neuen Fenster geöffnet

Payment gateway data breach Compromises 1.7M Credit Cards - Technijian

Wird in einem neuen Fenster geöffnet

5 Examples of Payment Processing Breaches to Learn From in 2025 - Payline Data

Wird in einem neuen Fenster geöffnet

Early Lessons from India’s Demonetization Experiment | Brookings

Wird in einem neuen Fenster geöffnet

2016 Indian banknote demonetisation - Wikipedia

Wird in einem neuen Fenster geöffnet

The economic and political consequences of India’s demonetisation - VoxDev

Wird in einem neuen Fenster geöffnet

India’s Demonetization Reduced Employment and Economic Activity - NBER

❓ Frequently Asked Questions

Why is cash important for freedom?

Cash enables payments without identification, without an app, and without an intermediary. This preserves financial privacy and gives individuals more sovereignty over their money.

What risks does a cashless society pose?

A cashless society increases the potential for surveillance, algorithmic profiling, and de-banking. It also makes people more dependent on banks, payment providers, and digital infrastructure.

How does cash protect against surveillance?

Cash leaves no digital record at the time of payment that can be linked with other information. This makes spending patterns, locations, and sensitive life circumstances much harder to analyze.

Why are digital ID and biometric systems problematic for payments?

If access to money depends on digital identity or biometric verification, people can be excluded if they lack the required infrastructure or fail verification. What is presented as financial inclusion can therefore become de facto exclusion.

How does cash affect card payment fees?

Cash remains a real alternative to Visa, Mastercard, and other payment networks, strengthening merchants’ bargaining power. Without cash, card and platform fees can rise more easily, which ultimately also burdens consumers.

Keep reading

More from this topicBaking Soda: Miracle Cure or Myth?

Baking soda is said to do many things: clean, help, protect — but what of that is true? We explain its effects, production, and history in an easy-to-understand way.

Mechanisms of Self-Learning AI Agents

My experiment with virtual & autonomous AI employees: cloning myself, working less, accomplishing more. An inside look at the background.

Paraguay Fish Guide - What Is There and How Good Is It?

Which fish from Paraguay are easy to digest? Our guide explains toxins, heavy metals, and omega-3s so you can make smarter choices.